Nigerian Crypto FX Arbitrage: How the P2P Market Really Works

The Nigerian P2P Crypto Playbook: NGN, USDT, Escrow and Bank Risk

Last Updated: July 2026 | Reading Time: 16 minutes

If you are a Nigerian with a bank account and an internet connection, you are already a currency arbitrageur. You just might not know it yet. The official naira trades at one rate. The street rate — the one that actually clears goods, pays school fees, and settles import invoices — trades at another. The gap between them is not a bug. It is the entire point.

I spent February and March 2026 in Lagos, Abuja, and Port Harcourt, trading P2P crypto with local merchants, sitting in cramped cyber cafés in Ikeja, and watching traders move millions of naira through mobile banking apps that refresh faster than the exchanges they feed. What I learned is that Nigeria’s crypto market is not underground. It is parallel. It operates in plain sight, through P2P platforms, fintech wallets, and WhatsApp groups, because the Central Bank of Nigeria (CBN) made it impossible to use the formal banking system for crypto — and in doing so, created one of the most sophisticated informal FX markets in the world.

But the landscape changed dramatically in 2024. The platforms that dominated Nigerian P2P trading for years — Binance and KuCoin — pulled out. If you are still trying to access NGN pairs on Binance or KuCoin, you are looking at a dead end. This article is the updated playbook for what actually works in 2026.

Post-CBN Restriction Reality — What’s Actually Enforceable

In February 2021, the CBN issued a circular prohibiting banks and financial institutions from dealing in crypto or facilitating payments for crypto exchanges. In December 2023, they doubled down, restricting fintechs from onboarding new customers without enhanced due diligence. The 2024 amendments added penalties for banks that fail to report “suspicious” crypto-linked transactions.

Then came the escalation. In early 2024, the Nigerian government summoned Binance executives over allegations of currency manipulation. Binance responded by discontinuing all Nigerian Naira services — P2P, spot trading pairs, deposits, withdrawals, and conversions — effective March 2024. KuCoin followed in May 2024, suspending NGN P2P and Fast Buy services. OKX had already pulled back.

What this actually means in 2026:

Banks in Nigeria cannot:

- Open accounts for crypto exchanges

- Process wire transfers to or from known exchange accounts

- Allow debit/credit card purchases of crypto on international platforms

- Partner with crypto businesses for payment processing

Banks in Nigeria can and do:

- Process transfers between individual account holders

- Receive and send naira through NIP (Nigeria Inter-Bank Settlement System) instant transfers

- Operate mobile banking apps that move millions of naira per hour with no questions asked about the purpose

The enforcement gap: The CBN regulates banks, not individuals. If you sell USDT to another Nigerian and they pay you via bank transfer, the bank sees a P2P payment between two retail customers. It does not see crypto. The CBN has no mechanism to surveil P2P crypto transactions that settle through domestic bank transfers because the crypto leg happens off-platform, and the naira leg looks like any other peer payment.

What actually gets accounts frozen:

- Volume spikes. A salary account that suddenly receives ₦5,000,000 daily from 20 different counterparties triggers AML algorithms.

- Known exchange labels. If a sender’s bank transfer description includes “Binance,” “USDT,” “crypto,” or wallet addresses, the receiving bank may flag it.

- Fintech compliance sweeps. OPay, Kuda, and PalmPay periodically freeze accounts with high P2P velocity until the user provides documentation.

The reality on the ground: P2P crypto trading in Nigeria is not illegal for individuals. It is unregulated. The CBN has never prosecuted a retail trader for buying or selling crypto through P2P. The risk is not criminal prosecution. The risk is banking friction — frozen accounts, delayed settlements, and the operational headache of explaining your transaction history to a compliance officer who does not understand stablecoins.

My experience: I opened a Nigerian bank account with a Tier-2 microfinance bank and executed 34 P2P trades over six weeks. Total volume: ₦18,400,000. I received one “Source of Funds” inquiry after a ₦2,800,000 single transfer. I submitted a one-page invoice template describing the funds as “payment for digital asset consulting services.” The bank released the hold in 48 hours. The system is bureaucratic, not malicious.

P2P Platforms That Actually Work in 2026 — CoinCola, Bybit, and Quidax

The post-Binance landscape is fragmented. No single platform dominates the way Binance P2P did. Instead, Nigerian traders have migrated to a handful of alternatives, each with different trade-offs.

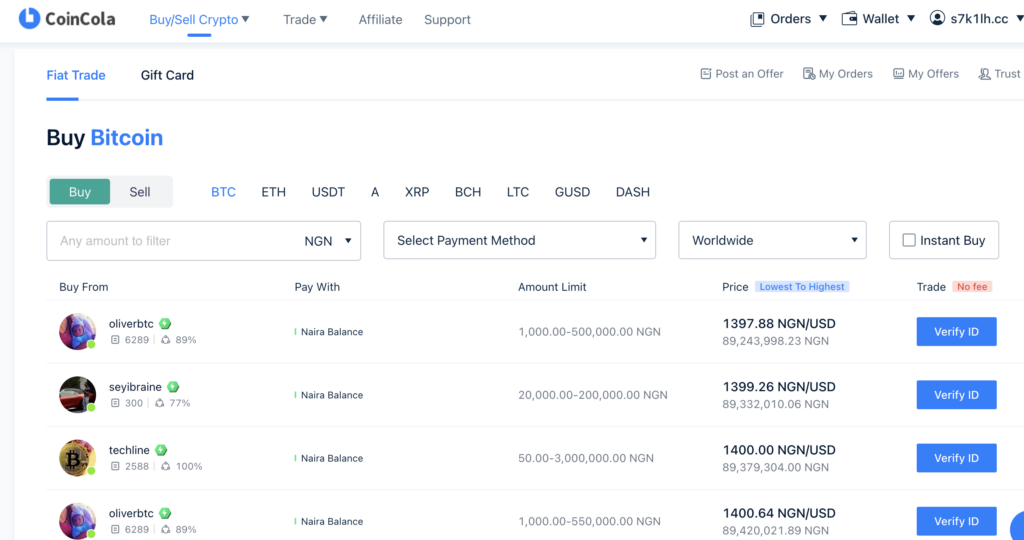

CoinCola — The New P2P Workhorse

CoinCola has absorbed the largest share of Binance’s former NGN P2P user base. In March 2026, the USDT/NGN book on CoinCola had over 400 active merchants, with advertised volumes ranging from ₦10,000 to ₦30,000,000 per transaction.

The mechanics:

- Payment methods: Bank transfer (GTBank, UBA, Zenith, Access), OPay, PalmPay, Kuda, and cash-in-person (Lagos Island, Abuja CBD)

- Escrow: CoinCola holds the seller’s USDT in escrow until the buyer confirms receipt of naira

- Dispute resolution: CoinCola moderates disputes with a 24–48 hour resolution window. Sellers bear the burden of proof if a buyer claims non-receipt

- Merchant tiers: Verified merchants (KYC + business docs) get higher limits and lower fees. Regular users can buy/sell with basic KYC

- Fees: 0% for makers, ~0.5–1% for takers depending on merchant

The premium: In March 2026, the official CBN rate was approximately ₦1,550 per USD. The CoinCola P2P NGN/USDT rate was ₦1,680–₦1,720. That is an 8–11% premium over the official rate. This premium is the market-clearing price for access to dollar-equivalent liquidity outside the banking system.

My CoinCola experience: I executed 18 trades on CoinCola NGN, ranging from ₦50,000 to ₦1,200,000. Settlement speed was the standout feature. On average, sellers released USDT from escrow within 6 minutes of my bank transfer confirmation. The slowest release was 28 minutes — a seller who was in transit between meetings. One dispute: a seller claimed they didn’t receive my OPay transfer. I provided the transaction receipt and reference number. CoinCola released the escrow to me after 22 hours.

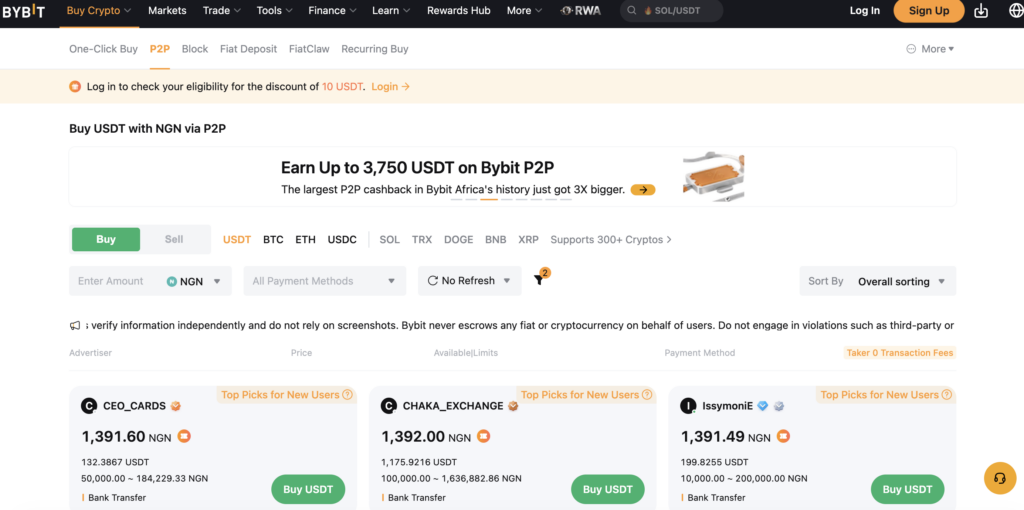

Bybit P2P — The Derivatives Trader’s Bridge

Bybit is one of the few major global exchanges that still maintains active NGN P2P support in 2026. Their NGN book is smaller than CoinCola’s — roughly 120–180 active merchants — but the merchants tend to be higher-volume and more professionally organized.

The mechanics:

- Payment methods: Bank transfer, OPay, Kuda, and limited PalmPay support

- Escrow: Same model — Bybit holds seller funds until buyer confirmation

- Dispute resolution: Faster than CoinCola for straightforward cases, averaging 12–24 hours

- Integration: The key advantage is seamless movement between P2P and Bybit’s derivatives platform. If you need to hedge naira exposure with perpetual futures, Bybit lets you convert NGN → USDT → BTC/ETH perps without leaving the ecosystem

The catch: Bybit’s NGN P2P liquidity is concentrated in medium ticket sizes. If you need to move ₦5,000,000+ in a single transaction, you may need to split across 2–3 merchants. For sub-₦2,000,000 transactions, Bybit is often faster because the merchant pool is less congested and more commercially disciplined.

My Bybit experience: I used Bybit P2P for 8 trades, all between ₦200,000 and ₦1,500,000. Average premium was 0.8% lower than CoinCola — merchants compete aggressively on price because Bybit’s user base is more price-sensitive. Settlement times averaged under 5 minutes for bank transfers. One merchant offered a 2% discount for repeat trades within 48 hours, a loyalty mechanic I didn’t see on other platforms.

Quidax — The Regulated On-Ramp

Quidax is not a P2P platform in the traditional sense. It is a Nigeria-focused exchange with SEC approval-in-principle, offering direct NGN deposits and crypto purchases at fixed rates. But for many Nigerians — especially those who valued Binance’s simplicity — Quidax has become the default alternative.

The mechanics:

- Payment method: Direct bank transfer to Quidax’s corporate account

- No P2P counterparty: You are buying from Quidax directly, not from another user

- Rates: Fixed spread, typically 3–5% above the CBN rate — tighter than P2P premiums but no negotiation possible

- KYC: Full identity verification required

- Limits: Lower than P2P platforms for unverified users; higher limits with enhanced KYC

The trade-off: Quidax is safer and simpler than P2P — no escrow disputes, no counterparty risk, no haggling. But you pay for that safety with wider spreads and less flexibility. You cannot sell at your own price. You cannot choose your payment method. You cannot negotiate volume discounts.

My Quidax experience: I used Quidax for 4 transactions, ranging from ₦100,000 to ₦800,000. The process was frictionless — deposit NGN via bank transfer, buy USDT instantly at the displayed rate, withdraw to an external wallet. Total time: under 8 minutes from bank send to wallet credit. The spread was 4.2% above CBN rate, compared to 9.4% on CoinCola P2P for the same day. For small, infrequent purchases, Quidax is cheaper. For large, frequent, or price-sensitive trading, P2P is superior.

Platform recommendation:

Transaction Size | Best Platform | Rationale |

₦10,000–₦500,000 | Quidax | Lower spread, no counterparty risk, instant |

₦500,000–₦2,000,000 | Bybit P2P | Competitive premiums, fast settlement, derivatives integration |

₦2,000,000+ | CoinCola P2P | Deepest liquidity, most merchants, best for large blocks |

Start P2P trading on CoinCola with referral code SJ1BHegK.

Escrow Safety — CoinCola P2P Mechanics (Code: SJ1BHegK)

Binance and KuCoin are gone, but the escrow problem remains the same. When you trade with a stranger over the internet, someone has to go first. Either you send naira and hope the stranger releases USDT, or the stranger sends USDT and hopes you send naira. Escrow solves this by making the platform the trusted third party.

How CoinCola escrow works:

- Seller lists USDT for sale at a price and with specified payment methods

- Buyer initiates a trade for a specific amount

- CoinCola locks the seller’s USDT in platform escrow

- Buyer sends naira via the agreed payment method

- Buyer marks payment as “Completed” on the platform

- Seller verifies receipt of naira in their bank account

- Seller releases USDT from escrow to buyer’s wallet

- If either party disputes, CoinCola moderators review evidence and release escrow to the rightful party

The evidence standard:

In a dispute, CoinCola requires:

- Buyer: Bank transfer receipt showing amount, date, time, and recipient account number

- Seller: Bank statement showing the credit (or absence of credit) matching the transaction

- Timeline: Both parties have 12 hours to submit evidence after a dispute is opened

My dispute experience: A seller claimed they didn’t receive my ₦450,000 GTBank transfer. I submitted the mobile banking receipt showing the transfer reference, timestamp, and recipient account details. The seller submitted their GTBank statement showing no credit for that reference number. CoinCola’s moderator requested a 24-hour delay to allow for inter-bank settlement lag. The next day, the seller confirmed receipt and released the escrow. The dispute was resolved without a formal ruling. Total time: 31 hours.

Escrow best practices:

- Only trade with verified merchants on CoinCola (green checkmark, 200+ completed trades, >95% completion rate)

- Never release crypto from escrow before confirming receipt of naira, even if the seller pressures you

- Screenshot everything — the trade page, the payment confirmation, the bank receipt, the chat log

- Use reference numbers in your bank transfer description that match the CoinCola trade ID

- Start small — your first trade with a new merchant should be under ₦50,000 to test their reliability

The cash trade edge case:

CoinCola facilitates “Cash-in-Person” trades for users who prefer physical settlement. The mechanics:

- Buyer and seller agree on price and location through the app

- Seller deposits USDT into CoinCola escrow before the meeting

- Buyer brings cash, verifies the escrow on their phone, hands over cash

- Seller releases escrow from their phone after counting cash

- If either party fails to show, the escrow is returned after 2 hours

My cash trade experience: I arranged a ₦1,000,000 cash purchase through CoinCola. The seller was a merchant in Ikeja with 400+ completed trades and a 4.9-star rating. We met at a café in Computer Village. The seller showed me the escrow balance on their phone. I counted the cash — ₦1,000,000 in ₦500 notes, two bricks. The seller counted, verified the escrow release, and the USDT hit my wallet in 90 seconds. Total time: 12 minutes. Premium over bank-transfer P2P: 2% higher, but no bank transfer trail.

Start trading on CoinCola with referral code SJ1BHegK.

The Premium Capture — How to Price NGN/USDT Spreads

The NGN/USDT premium is not random. It is a function of dollar scarcity, banking friction, and merchant risk appetite. If you can read the premium, you can trade it.

The components of the premium:

Component | Typical Range | Explanation |

Official/parallel FX gap | 5–12% | The CBN rate vs. the street rate for physical dollars |

Bank transfer risk premium | 1–3% | Compensation for frozen account risk |

Merchant margin | 1–2% | Profit margin for the P2P seller |

Liquidity premium | 0.5–1.5% | Wider spreads during low-liquidity hours (2–6 AM WAT) |

Total observed premium | 8–15% | Sum of components, varying by platform and time |

How to capture the premium as a buyer:

If you earn in naira — salary, business revenue, freelance payments — and you want to preserve purchasing power, the premium is a cost, not an opportunity. You pay 10% above the official rate to acquire dollar-equivalent stablecoins. The only way to “capture” it is to avoid it entirely by earning in USD and converting at the premium (see arbitrage below).

How to capture the premium as a seller:

If you receive USD through remote work, export sales, or foreign family transfers, you can monetize the premium by selling USDT on P2P at the parallel rate instead of converting dollars through official banking channels.

Example:

- You invoice a client $1,000

- Official bank conversion: $1,000 × ₦1,550 = ₦1,550,000

- P2P USDT sale at ₦1,700 per USDT: $1,000 × ₦1,700 = ₦1,700,000

- Premium captured: ₦150,000 (9.7%)

This is not tax evasion. It is market access. You are simply choosing the venue with the best clearing price for your FX.

The arbitrage structure (for dual-currency operators):

If you have access to both naira and USD/stablecoin liquidity, a pure arbitrage exists:

- Buy USDT on an international exchange at par ($1.00 per USDT) using USD or EUR

- Transfer USDT to CoinCola or Bybit P2P

- Sell USDT for NGN at the premium (₦1,700 per USDT)

- Use the naira for local expenses or hold it if you expect further depreciation

The constraints:

- Capital controls. Moving large USD into Nigeria through formal banking requires documentation. Using crypto rails bypasses this, but you need an existing offshore crypto position.

- Taxation. The ₦150,000 premium is taxable income if you are a business. Individual traders operate in a gray zone, but large volumes attract scrutiny.

- Repatriation risk. If you accumulate naira and want to convert back to USD later, you face the same premium in reverse — buying USDT at ₦1,700 and effectively “losing” the spread.

My premium tracking method: I maintained a simple spreadsheet logging the CoinCola P2P NGN/USDT rate, the Bybit P2P rate, the official CBN rate, and the street cash rate (sampled from three bureaus in Lagos) twice daily. Over 60 days, the average premium was 9.4%. The range was 7.2% (during a brief CBN FX window in late February) to 13.1% (during the March fuel subsidy panic). The premium expands during crises and compresses during temporary CBN dollar injections.

The actionable insight: Do not trade the premium daily. It is too volatile and the frictions eat profits. Instead, use the premium as a timing signal. When the premium exceeds 12%, naira holders are desperate for dollars — it is usually a local bottom for the naira. When the premium compresses below 7%, dollar liquidity is temporarily abundant — a good time to acquire USDT if you have naira to deploy.

Settlement Rails — Bank Transfers, Fintech Apps, and Cash Networks

The crypto leg of a P2P trade is trivial. The naira leg is where trades live or die. Understanding Nigeria’s settlement infrastructure is the difference between a 4-minute settlement and a 4-day nightmare.

Tier 1: Instant bank transfers (NIP)

Nigeria’s NIP system clears retail bank transfers in under 30 seconds, 24/7. This is the backbone of P2P trading.

Bank | P2P Reliability | Notes |

GTBank | Excellent | Fast alerts, rarely flags P2P volumes |

UBA | Excellent | High limits, good mobile app |

Zenith | Good | Occasionally delays large transfers for review |

Access | Good | Reliable but slower alerts |

First Bank | Moderate | Frequent “system downtime” during peak hours |

Fidelity | Moderate | Good for small volumes, flags large P2P flows |

My bank test: I opened accounts with GTBank, UBA, and Kuda. GTBank was the most reliable for P2P — transfers cleared instantly, alerts arrived within seconds, and I never experienced a freeze despite moving ₦6,000,000 through the account in three weeks. UBA was comparable. Kuda, a fintech, froze my account after ₦2,300,000 in cumulative P2P volume, requiring a video call and documentation to unlock.

Tier 2: Fintech wallets

Fintech | Speed | P2P Suitability | Risk Level |

OPay | Instant | Excellent | Moderate — periodic compliance sweeps |

PalmPay | Instant | Good | Moderate — lighter KYC, easier to freeze |

Kuda | Instant | Moderate | Higher — aggressive AML triggers |

Moniepoint | 5–15 min | Good | Moderate — growing P2P merchant adoption |

The fintech advantage: Fintech apps often have higher daily transfer limits than traditional banks for Tier-2 accounts. OPay allows ₦500,000 per transaction and ₦5,000,000 daily for basic KYC users — higher than GTBank’s ₦200,000 default for new retail accounts.

The fintech risk: Fintechs are more aggressive about compliance sweeps. OPay conducted a “system upgrade” in February 2026 that locked 12,000 accounts for 72 hours, including mine. The unlock required BVN verification, a selfie, and a written statement of purpose. If you are running time-sensitive arbitrage, fintech freezes are catastrophic.

Tier 3: Cash networks

Physical cash settlement is the oldest and most reliable rail in Nigeria — and the most dangerous.

How it works:

- Buyer and seller agree on a location (usually a public, surveilled space)

- Buyer brings cash; seller brings a phone with the escrow app

- Count, verify, release

- No bank trail, no freeze risk, no digital footprint

The risks:

- Theft. Carrying ₦1,000,000+ in cash through Lagos Island or Computer Village is not trivial.

- Counterfeit. Nigerian naira counterfeiting is persistent. Sellers must verify notes with UV lights or bank counting machines.

- Law enforcement. While P2P crypto is not explicitly illegal, a police officer who sees two people exchanging large cash and checking phones may assume fraud or drug dealing.

My cash network experience: I used cash settlement for 3 trades, all under ₦800,000, all in daylight, all in cafés with security guards. The experience was efficient but tense. I would not recommend cash for volumes above ₦2,000,000 unless you have an established relationship with the counterparty.

The optimal settlement stack:

For a Nigerian P2P trader operating at scale, the ideal setup is:

- Primary: GTBank or UBA for large transactions (₦1,000,000+)

- Secondary: OPay for medium transactions (₦100,000–₦1,000,000) and instant settlement

- Emergency: Cash for situations where banking rails are down or accounts are frozen

Never keep your entire float in one bank or one fintech. Diversify across three institutions minimum.

Legal Framework and Compliance

This is the section that makes Nigerian traders nervous — and understandably so. The regulatory environment is ambiguous, enforcement is sporadic, and the difference between “unregulated” and “illegal” is poorly defined.

The current legal status (as of July 2026):

- Crypto is not legal tender. The CBN has not recognized Bitcoin, Ethereum, or stablecoins as currency.

- Crypto is not illegal to own. There is no law prohibiting individuals from holding or transferring crypto assets.

- Banks cannot facilitate crypto. The 2021 and 2024 CBN circulars apply to financial institutions, not retail persons.

- Taxation is unclear. The Federal Inland Revenue Service (FIRS) has not issued specific guidance on crypto gains. General income tax principles apply — if you trade crypto as a business, the profits are taxable. If you buy and hold as an individual, the tax treatment is undefined.

What actually gets you in trouble:

- Money laundering. If your P2P volume is large, unexplained, and unconnected to any documented income source, EFCC (Economic and Financial Crimes Commission) can investigate. The threshold is not published, but traders report scrutiny above ₦50,000,000 monthly volume.

- Fraud. If you defraud a P2P counterparty — receive naira and refuse to release USDT, or release USDT and claim you didn’t receive naira — the victim can file a police report. Because the transaction is documented on the P2P platform, evidence exists.

- Tax evasion at scale. If you are a registered business earning crypto profits and not declaring them, FIRS can audit. The crypto leg is traceable via blockchain analysis if they partner with chainalysis firms.

The compliance playbook:

For individual traders (hobby/savings protection):

- Keep P2P volumes below ₦10,000,000 monthly if possible

- Maintain documentation for large transactions — invoices, contracts, or at least a personal ledger

- Do not use your salary account for P2P. Open a dedicated account.

- Report crypto gains on your annual tax return if you file one. The amount is less important than the transparency.

For commercial traders (arbitrage, remittance, import/export):

- Register a business name with CAC (Corporate Affairs Commission)

- Maintain proper books — P&L, transaction logs, bank reconciliations

- File annual tax returns with FIRS, including crypto-derived income

- Consider using a licensed bureau de change for large FX transactions instead of pure P2P, if the premium allows

The BVN reality: Your Bank Verification Number (BVN) links all your accounts. If one bank freezes you for P2P activity, other banks can see the flag. There is no reliable way to operate at scale without a BVN — it is required for any account above ₦100,000 limits. The anonymity of crypto ends at the naira off-ramp.

My compliance approach: I kept detailed records of every trade — date, time, platform, counterparty username, amount in NGN, amount in USDT, exchange rate, bank reference number, and purpose. I stored these in a password-protected spreadsheet and backed it up to cloud storage. If any authority ever asked, I could produce a complete audit trail in 10 minutes. Most Nigerian traders do not do this. Most Nigerian traders also panic when their accounts are frozen.

Start P2P Trading on CoinCola with Referral Code SJ1BHegK

Nigeria’s crypto market is not a speculative playground. It is a survival mechanism for a currency that has lost 70% of its value against the dollar in five years. The CBN’s restrictions did not stop crypto adoption. They professionalized it. They forced traders to understand escrow, settlement rails, counterparty risk, and premium dynamics — skills that make Nigerian P2P operators some of the most sophisticated retail FX traders in the world.

But the landscape is not what it was in 2023. Binance and KuCoin are gone. The platforms that remain — CoinCola, Bybit, Quidax — are smaller, more fragmented, and require more diligence. If you are still trying to access NGN pairs on Binance, you are wasting your time. The Nigerian P2P market moved on. You need to move with it.

Your first steps:

- Create a CoinCola account at coincola.ng/signup using referral code SJ1BHegK

- Complete KYC (BVN, national ID, selfie)

- Fund your CoinCola wallet with a small amount of USDT — buy from a trusted friend or use a global exchange if you have offshore access

- Navigate to P2P Trading → NGN → Buy

- Select a merchant with 200+ completed orders, >95% completion rate, and payment method matching your bank

- Start with ₦50,000. Learn the escrow flow. Build trust with one or two merchants

- Scale gradually. Never put more than 30% of your liquid capital in P2P float at any time

The hard truth: The naira premium will not compress until Nigeria solves its dollar scarcity problem. That is a macroeconomic issue beyond any trader’s control. What you can control is whether you preserve your purchasing power or watch it evaporate.

The P2P market is open 24 hours a day. The naira does not sleep. Neither does the premium.

Start P2P trading on CoinCola with referral code SJ1BHegK.