The Japanese Yen carry trade unwind is the primary catalyst for high-beta altcoin flash crashes in 2026. When the Bank of Japan (BOJ) tightens monetary policy, forced JPY repatriation triggers cascading margin calls, instantly liquidating leveraged altcoin positions. To survive, you must short altcoin beta when USD/JPY breaks structural support.

For years, retail crypto traders have operated under a dangerously incomplete macroeconomic framework. They watch the US Federal Reserve, track US CPI prints, and monitor Bitcoin dominance, completely ignoring the most critical source of global leveraged liquidity: the Japanese Yen.

In 2026, the crypto market is not merely a reflection of US dollar liquidity; it is deeply entangled with the cross-currency basis swaps and prime brokerage margin requirements of the Japanese carry trade. When the Bank of Japan (BOJ) shifts its monetary policy, the resulting unwinding of trillions of dollars in Yen-funded positions does not just cause a “market correction.” It triggers violent, algorithmic flash crashes that specifically target high-beta altcoins.

At Decentralised News, our mandate is to provide institutional-grade intelligence that reduces your risk. People do not buy financial tools to hear comforting narratives about decentralized utopias; they buy them to navigate complex, interconnected global markets and protect their capital from structural liquidation events. By understanding the exact mechanics of the Yen carry trade and its transmission mechanism into altcoin beta, you transition from a reactive retail participant getting liquidated on scam wicks to a proactive operator front-running global margin calls.

Below, we dissect the mathematical reality of the 2026 BOJ pivot, the hidden structural truths of prime brokerage liquidations, and the exact execution strategies required to trade the carry trade unwind without falling victim to the cascade.

1. The Mechanics of the Yen Carry Trade and the 2026 BOJ Pivot

To understand why altcoins flash crash during a Yen unwind, you must first understand the sheer scale and mechanics of the carry trade itself. This is not a niche forex strategy; it is the foundational plumbing for global risk asset leverage.

The Anatomy of the Carry Trade

The carry trade relies on the interest rate differential between a low-yielding currency and a high-yielding asset. Historically, Japan has maintained near-zero or negative interest rates. Institutional investors, hedge funds, and even retail market makers borrow Japanese Yen (JPY) at minimal cost (e.g., 0.1% to 0.5%), convert it to US Dollars (USD), and deploy that capital into higher-yielding assets.

In the crypto ecosystem, this JPY liquidity does not just sit in US Treasuries. It flows into crypto market-making firms, decentralized finance (DeFi) yield aggregators, and leveraged altcoin trading desks. The “carry” is the profit made from the spread between the cheap JPY borrowing cost and the high crypto yield or capital appreciation.

The 2026 BOJ Reality: The Death of Yield Curve Control

The fatal flaw of the carry trade is its sensitivity to the derivative of the interest rate differential, not just the absolute rate. In 2024, we witnessed a preview of this when the BOJ briefly hinted at tightening, causing the “Black Monday” crypto flash crash.

In 2026, the BOJ’s Yield Curve Control (YCC) is effectively dead. Japanese inflation has structurally normalized above the 2% target, forcing the BOJ to continue normalizing rates. When the BOJ hikes rates from 0.5% to 1.0%, the absolute rate is still low, but the rate of change is massive.

Furthermore, as JPY interest rates rise, the JPY strengthens against the USD. This creates a double-whammy for carry trade participants:

- Higher Borrowing Costs: The cost to roll over JPY loans increases.

- FX Losses: The underlying collateral (denominated in USD or crypto) loses value when converted back to JPY to repay the principal.

When this dynamic shifts, the trade becomes unprofitable, and participants must unwind their positions. They must sell their USD and crypto assets, buy JPY, and repay the loans. This forced repatriation of capital is the mathematical trigger for altcoin flash crashes.

2. The Transmission Mechanism: How JPY Strength Liquidates Altcoin Beta

Retail traders assume that when macro liquidity tightens, all crypto assets drop equally. This is empirically false. The carry trade unwind specifically and violently targets Altcoin Beta. To understand why, we must look at the hidden structural truth of prime brokerage margin requirements.

The Prime Brokerage Margin Call Cascade

Institutional crypto funds do not trade with their own cash; they use prime brokers and institutional lending desks. These desks accept crypto assets (like ETH, SOL, and high-cap altcoins) as collateral for JPY or USD margin loans.

When the USD/JPY exchange rate drops rapidly (meaning the Yen is strengthening), the USD value of the fund’s collateral remains the same, but the JPY value of that collateral drops. If a fund has borrowed 1 billion JPY against $7 million worth of SOL, and the JPY strengthens by 10%, the fund is suddenly under-collateralized.

The prime broker issues a margin call. The fund has 24 hours (or sometimes minutes, in the case of automated risk engines) to post more collateral or reduce their loan. Because raising new JPY is expensive, they choose to reduce the loan. To do this, they must sell their collateral.

Why Altcoins Bear the Brunt of the Liquidation

Why do they sell altcoins instead of Bitcoin? Because of liquidity and beta.

- Bitcoin has deep institutional liquidity. Selling $10 million of BTC causes minimal slippage.

- Altcoins have thinner order books and higher beta.

When a fund needs to raise cash instantly to cover a JPY margin call, algorithmic execution engines are programmed to sell the assets with the highest immediate liquidity and highest beta to maximize the cash extracted per unit of market impact. High-beta altcoins (like Solana, Avalanche, and Layer 1 tokens) are dumped first.

This creates a cascading effect:

- Fund A sells SOL to cover JPY margin.

- SOL price drops 5%.

- This drop triggers the stop-losses and liquidation engines of highly leveraged retail traders on crypto exchanges.

- The forced selling from retail liquidations pushes SOL down another 10%.

- Fund B’s collateral is now under-collateralized, triggering their margin call, forcing them to sell more altcoins.

This is the mechanics of a Flash Crash. It is not driven by a change in the fundamental value of the altcoin; it is driven by a structural, mechanical necessity to raise JPY to cover cross-currency margin deficits.

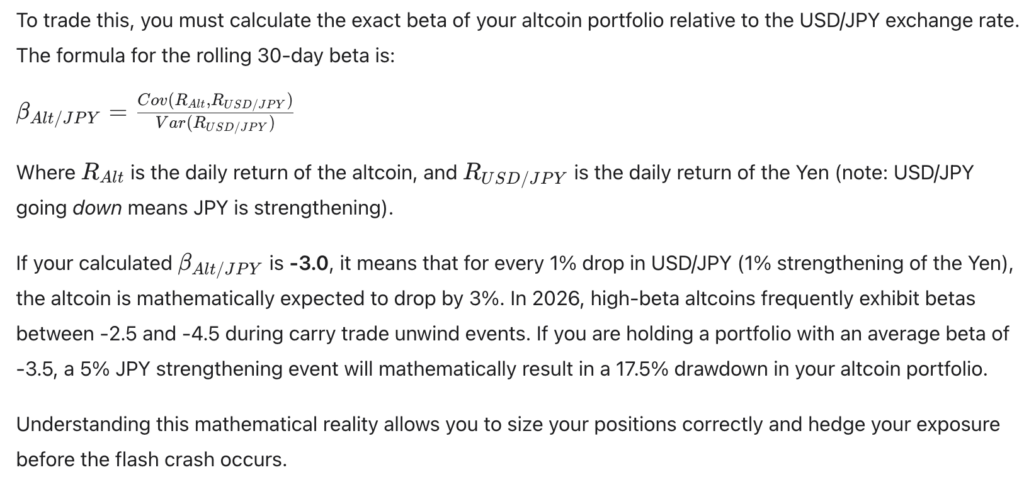

Calculating Altcoin Beta to USD/JPY

3. Identifying the Flash Crash: Order Book Dynamics and Liquidation Heatmaps

Knowing the macro thesis is only 20% of the battle; the other 80% is execution and risk management. The crypto market in 2026 is plagued by algorithmic stop-hunting. During a carry trade unwind, the order book dynamics shift dramatically, creating “scam wicks” that liquidate over-leveraged traders in minutes.

The Vacuum of Liquidity

When a major carry trade unwind begins, institutional market makers widen their bid-ask spreads to protect themselves from the extreme volatility. The order book becomes incredibly thin.

In a normal market, a $5 million sell order on an altcoin might move the price by 0.5%. During a carry trade unwind, because the market makers have pulled their bids, that same $5 million order can move the price by 3% to 5%. This thin liquidity is what causes the vertical, parabolic drops characteristic of a flash crash.

Mapping the Liquidation Clusters

To survive and profit from these events, you must map the liquidation clusters. Liquidation heatmaps show exactly where highly leveraged long positions are sitting.

When the USD/JPY begins to break down, you must look at the altcoin liquidation heatmaps. If you see $500 million worth of 10x and 25x long liquidations clustered just 3% below the current market price, you know exactly where the price is going to gravitate. The algorithms will push the price down to that exact level to trigger the cascade, absorb the cheap collateral, and then reverse the price.

Execution Mechanics: Shorting the Cascade

When the macro trigger (BOJ policy shift) aligns with the technical trigger (USD/JPY breaking key support) and the structural trigger (massive altcoin long liquidation clusters below), the probability of a flash crash approaches certainty.

This is the exact moment to deploy short positions. However, you cannot use market orders. In a thin order book, a market short order will suffer catastrophic slippage. You must use limit orders placed exactly at the liquidation cluster levels, or use algorithmic execution tools like TWAP (Time-Weighted Average Price) to scale into your short position without moving the market against yourself.

When you need to execute high-leverage short positions during extreme volatility, you require an exchange with deep liquidity, robust matching engines, and advanced order types that do not freeze during market stress. Short altcoin beta on MEXC using code 16yJL to access their high-frequency trading infrastructure, ensuring your short entries and exits are executed with precision, allowing you to capture the violent mean reversion of the flash crash without suffering from platform lag or slippage. 4. The Mathematical Framework: Hedging Altcoin Portfolios Against JPY Volatility

For institutional operators and high-net-worth individuals who cannot simply close their altcoin positions and move to stablecoins, hedging against JPY volatility is a mathematical necessity. Relying on “hope” during a carry trade unwind is a guaranteed path to capital destruction.

Delta-Neutral Hedging with Perpetual Futures

The most direct way to hedge altcoin beta is to short the corresponding perpetual futures. If you hold $100,000 worth of Solana (SOL) spot, and the SOL/USD/JPY beta is -3.0, a 5% JPY strengthening will cost you $15,000 in spot value.

To neutralize this, you must open a short position on the SOL perpetual future. The exact hedge ratio is calculated as:

By maintaining a delta-neutral position, you eliminate your exposure to the directional price movement of the altcoin, effectively isolating your portfolio from the carry trade unwind. You can then collect the funding rate (if the market is overly bearish and funding is negative) or simply preserve your capital until the macro environment stabilizes.

Options Hedging: The Asymmetric Advantage

While futures hedging is exact, it requires constant adjustment as the beta changes and ties up margin. Options provide an asymmetric hedge.

During a carry trade unwind, implied volatility (IV) on altcoin options skyrockets. If you wait until the flash crash is happening to buy puts, you will pay a massive volatility premium. The institutional edge is to buy Out-of-the-Money (OTM) put options before the BOJ announcement or when the USD/JPY is approaching major technical support.

- The Strategy: Allocate 1% to 2% of your portfolio’s value to buy 1-month OTM puts on high-beta altcoins (like SOL or AVAX).

- The Outcome: If the carry trade does not unwind, you lose the 1-2% premium (a known, capped risk). If the carry trade unwinds and triggers a 20% flash crash, the value of those put options will increase by 500% to 1,000% due to the combination of delta expansion and vega (volatility) expansion. The profits from the puts will more than offset the drawdown in your spot altcoin portfolio.

The Stablecoin Yield Offset

Another layer of risk reduction is to ensure that the un-hedged portion of your portfolio is generating “Real Yield” that can offset minor drawdowns. By moving a portion of your capital into tokenized Treasuries or delta-neutral DeFi strategies, you create a steady cash flow that acts as a buffer against the volatility of the carry trade unwind.

Decentralised News emphasizes that capital preservation is paramount. By combining delta-neutral futures hedging, asymmetric options protection, and real yield generation, you reduce the risk of a catastrophic drawdown, ensuring your portfolio survives the violent interim volatility of the 2026 macro cycle.

5. The 2026 Playbook: 4 Exact Setups to Trade the Carry Trade Unwind

To operationalize the Yen carry trade thesis, you need a strict, rules-based playbook. Below are the four exact setups that institutional macro traders use to extract alpha and protect capital during JPY liquidity shifts in 2026.

Setup 1: The BOJ Surprise Hike (The Initial Shock)

- Macro Condition: The BOJ unexpectedly hikes rates by 25bps or signals an accelerated reduction in JGB (Japanese Government Bond) purchases.

- Technical Trigger: USD/JPY gaps down more than 2% in the Asian session.

- Action: Immediately reduce spot altcoin exposure by 50%. Do not wait for the US session. The initial shock will trigger the first wave of algorithmic margin calls.

- Risk Management: Move the raised capital into short-term stablecoin yields. Do not attempt to catch the falling knife in the first 4 hours.

Setup 2: The USD/JPY Technical Breakdown (The Trend Confirmation)

- Macro Condition: The BOJ is in a confirmed tightening cycle. US-Japan yield differential is compressing.

- Technical Trigger: USD/JPY breaks and closes below the 200-day Simple Moving Average (SMA) on the daily chart.

- Action: Aggressively short high-beta altcoins using perpetual futures. The macro trend is confirmed, and the structural unwind will persist for weeks.

- Risk Management: Use 3x leverage. Set trailing stops based on the 4-hour Average True Range (ATR). If USD/JPY reclaims the 200-day SMA, invalidate the thesis and cover the shorts.

Setup 3: The Altcoin Liquidation Cascade (The Flash Crash Short)

- Macro Condition: USD/JPY is in a strong downtrend.

- Technical Trigger: Liquidation heatmaps show massive clusters of retail long liquidations 5% to 8% below the current altcoin price. Order book depth is thinning.

- Action: Place limit short orders exactly at the liquidation cluster levels. When the price wicks down to trigger the cascade, your orders will be filled at the absolute bottom of the wick.

- Risk Management: Immediately take profit (50% to 100% of the position) as soon as the price reclaims the pre-wick support level. Flash crash wicks reverse violently; do not hold the short into the bounce. Execute these precision wick-shorts on MEXC using code 16yJL to leverage their deep liquidity and advanced limit-order routing.

Setup 4: The Post-Unwind Mean Reversion (The Bottom Fishing)

- Macro Condition: The carry trade unwind has reached a climax. The BOJ pauses its rhetoric to let the market stabilize. USD/JPY hits a major historical support level (e.g., 135.00 or 140.00).

- Technical Trigger: The RSI on the daily USD/JPY chart drops below 30 (extreme oversold). Altcoin funding rates turn deeply negative (meaning the market is heavily short).

- Action: Begin scaling out of shorts and deploying spot capital into high-conviction altcoins. The margin calls have been satisfied, the forced selling is over, and the assets are mathematically oversold.

- Risk Management: Keep leverage at 1x. This is a mean-reversion trade, not a new bull trend. Take profits when the altcoin returns to its pre-crash moving averages.

Conclusion: Mastering the Global Liquidity Plumbing

The era of trading altcoins in a vacuum, ignoring global macroeconomic plumbing, is over. In 2026, the crypto market is a highly integrated component of the global financial system, and its highest-beta assets are inextricably linked to the Japanese Yen carry trade.

The BOJ’s monetary policy is not just a forex concern; it is the master switch for altcoin liquidity. By understanding the mechanics of cross-currency margin calls, calculating the exact beta of your portfolio to USD/JPY, and executing precise hedges during liquidation cascades, you protect your capital from the violent flash crashes that destroy retail traders.

Decentralised News exists to provide you with this institutional-grade clarity. We do not deal in hype; we deal in the structural realities of global finance. The Yen carry trade unwind is a mechanical certainty when the BOJ pivots. The only question is whether you will be the one front-running the margin calls, or the retail liquidity being liquidated to cover them. Master the plumbing, respect the beta, and secure your financial sovereignty in the 2026 macro cycle.

Frequently Asked Questions (FAQ)

1. What is the Japanese Yen carry trade and how does it affect crypto?

The Yen carry trade involves borrowing Japanese Yen at low interest rates to invest in higher-yielding assets, including crypto. When the Bank of Japan (BOJ) raises rates or the Yen strengthens, the trade becomes unprofitable. Investors must sell their assets (like altcoins) and buy Yen to repay loans, creating massive selling pressure that triggers flash crashes in high-beta crypto assets.

2. Why do altcoins crash harder than Bitcoin during a Yen carry trade unwind?

Altcoins have a much higher “beta” (volatility and sensitivity to liquidity) than Bitcoin. When institutional funds face margin calls due to Yen strengthening, their prime brokers require immediate USD collateral. Algorithms are programmed to sell the most liquid, highest-beta assets first to raise cash quickly, resulting in altcoins bearing the brunt of the forced liquidation cascade.

3. How can I calculate my altcoin portfolio’s risk to the Japanese Yen?

You calculate the risk by determining the “Altcoin Beta to USD/JPY” using the formula: Covariance of the altcoin’s daily returns and USD/JPY’s daily returns, divided by the variance of USD/JPY’s returns. A beta of -3.0 means that for every 1% the Yen strengthens (USD/JPY drops 1%), your altcoin is mathematically expected to drop by 3%.

4. What are the best strategies to hedge an altcoin portfolio against a carry trade unwind?

The most effective strategies include: 1) Delta-neutral hedging by shorting altcoin perpetual futures to offset spot exposure, 2) Buying Out-of-the-Money (OTM) put options before the BOJ announcement to profit from the volatility spike and price drop, and 3) Rotating a portion of the portfolio into stablecoin yields or tokenized Treasuries to generate a cash-flow buffer against drawdowns.

5. How do I spot and trade the “flash crash” wicks during a Yen unwind?

Flash crashes are caused by thin order books and cascading liquidations. You can spot them by monitoring liquidation heatmaps for massive clusters of retail long positions below the current price, combined with a breakdown in the USD/JPY exchange rate. To trade it, place limit short orders exactly at the liquidation cluster levels, and take profit immediately once the price reclaims the pre-wick support, avoiding the violent mean-reversion bounce.